Modern Debt Management Strategies for 2026: Your Complete Guide

Drowning in debt? Rising interest rates making it harder to keep up? You're not alone and you're not powerless. This comprehensive guide reveals the modern strategies that actually work to help you take control and become debt-free in 2026.

Why Debt Management Matters More Than Ever in 2026

Debt management is more important than ever in 2026, as rising interest rates and economic uncertainty put pressure on household budgets. Whether you're dealing with credit card debt, student loans, or other financial obligations, using smart strategies can help you regain control and work toward a debt-free future.

The economic landscape has shifted dramatically. Interest rates remain elevated compared to the past decade, credit card APRs average 20-25%, and everyday expenses continue climbing. This perfect storm makes carrying debt more expensive and more dangerous to your financial health than at any point in recent history.

But here's the good news: modern debt management strategies have evolved too. With the right approach, you can tackle debt faster, smarter, and with less stress than previous generations. This guide will show you exactly how.

If you're struggling with rising costs while managing debt, our guide on how young professionals can beat rising costs in 2026 provides additional context and strategies for navigating today's economic challenges.

Understanding Good Debt vs. Bad Debt: The Foundation

Not all debt is created equal. Understanding the difference between good debt and bad debt is crucial to making smart financial decisions and prioritizing your payoff strategy.

Good Debt: Investments in Your Future

Good debt typically has three characteristics:

- Low interest rates (generally under 6-8%)

- Increases your net worth or earning potential over time

- Tax advantages (in some cases)

Examples of good debt:

- Mortgages: Building equity in real estate while providing housing

- Student loans: Investing in education that increases earning potential

- Business loans: Funding ventures that generate income

- Low-interest auto loans: Transportation necessary for work (when kept reasonable)

Important caveat: Even "good" debt becomes bad debt if you overborrow. A $300,000 mortgage on a $50,000 salary or $200,000 in student loans for a $40,000/year career are examples of good debt gone wrong.

Bad Debt: The Wealth Killer

Bad debt has opposite characteristics:

- High interest rates (typically 15%+ APR)

- Finances depreciating assets or consumption

- No tax benefits

Examples of bad debt:

- Credit card debt: Especially for discretionary purchases at 20-25% APR

- Payday loans: Predatory interest rates of 400%+ APR

- High-interest personal loans: Used for consumption, not investment

- Retail store credit cards: Often 25-30% APR for clothing and electronics

- Car title loans: Extremely high rates risking vehicle loss

Your Priority: Attack Bad Debt First

Focus first on paying down high-interest, non-essential debts to reduce your overall financial burden. Bad debt costs you exponentially more over time and provides zero benefit to your financial future.

Example of bad debt's real cost:

$5,000 credit card balance at 22% APR, paying minimum payments only:

- Time to pay off: 15+ years

- Total interest paid: $7,000+

- Total cost: $12,000 for a $5,000 purchase

This is why aggressive bad debt elimination should be your financial priority after building a starter emergency fund. Speaking of which, before tackling debt aggressively, you need at least $1,000 in emergency savings. Learn how to build an emergency fund fast, even on a tight budget.

Key Debt Management Strategies That Actually Work

Now that you understand debt prioritization, let's dive into the proven strategies that will help you eliminate it efficiently.

1. Create a Realistic Budget: Your Debt-Fighting Foundation

A clear budget is the foundation of effective debt management. Track your income and expenses to identify areas where you can cut back and redirect money toward debt repayment.

Why budgeting matters for debt payoff:

- Reveals exactly how much you can allocate to debt monthly

- Identifies spending leaks that could become debt payments

- Prevents new debt accumulation while paying off existing debt

- Creates accountability and tracking for progress

The debt-crushing budget framework:

Phase 1: Starter Emergency Fund (1-2 months)

- Save $1,000 as fast as possible

- Pay minimums on all debts

- Cut non-essentials temporarily

Phase 2: Aggressive Debt Payoff (6-24 months depending on debt amount)

- 50-60% Needs: Housing, utilities, transportation, groceries, insurance

- 10-20% Wants: Minimal discretionary spending (temporary sacrifice)

- 30-40% Debt Payments: Maximized debt elimination

Phase 3: Full Emergency Fund (After high-interest debt is gone)

- Build 3-6 months of expenses

- Resume more balanced want spending

- Continue paying off remaining low-interest debt

Need help creating your budget? Our comprehensive guide on how to create a simple monthly budget that works for you walks you through the entire process step-by-step.

2. Choose Your Payoff Method: Avalanche vs. Snowball

Two proven methods dominate debt payoff strategies. Both work you just need to pick the one that matches your personality and motivation style.

The Debt Avalanche Method: Mathematical Optimization

How it works: Pay off debts with the highest interest rates first, regardless of balance. This reduces the total interest you'll pay over time.

Step-by-step process:

- List all debts by interest rate (highest to lowest)

- Pay minimum payments on everything

- Throw all extra money at the highest-rate debt

- Once paid off, roll that payment into the next highest rate

- Repeat until debt-free

Example:

- Credit Card A: $4,000 at 24% APR → Target first

- Credit Card B: $2,500 at 18% APR → Target second

- Personal Loan: $5,000 at 12% APR → Target third

- Student Loan: $10,000 at 5% APR → Target last

Pros:

- Saves the most money on interest

- Mathematically fastest payoff

- Reduces total debt cost by hundreds or thousands

Cons:

- May take longer to see first debt eliminated

- Requires discipline and patience

- Less psychological "wins" early on

Best for: Analytically-minded people who can stay motivated without frequent wins; those with significant interest rate differences between debts.

The Debt Snowball Method: Psychological Momentum

How it works: Focus on paying off the smallest debts first, regardless of interest rate, to build momentum and motivation.

Step-by-step process:

- List all debts by balance (smallest to largest)

- Pay minimum payments on everything

- Throw all extra money at the smallest balance

- Once paid off, roll that payment into the next smallest

- Celebrate each elimination as motivation

Example:

- Store Card: $500 at 26% APR → Target first

- Credit Card B: $2,500 at 18% APR → Target second

- Credit Card A: $4,000 at 24% APR → Target third

- Personal Loan: $5,000 at 12% APR → Target fourth

- Student Loan: $10,000 at 5% APR → Target last

Pros:

- Quick wins boost motivation dramatically

- See accounts eliminated faster

- Simplifies your debt picture quickly

- Builds confidence and momentum

Cons:

- May pay slightly more in total interest

- Mathematically less efficient

- Could take a few months longer overall

Best for: People who need motivation and quick wins; those with similar interest rates across debts; anyone who's struggled to stick with debt payoff before.

Which Method Should You Choose?

Choose Avalanche if:

- You have significant interest rate spreads (e.g., 24% vs. 8%)

- You're disciplined and data-driven

- Saving maximum money is your priority

- You can stay motivated without frequent wins

Choose Snowball if:

- You need psychological wins to stay motivated

- Interest rates are relatively similar

- You've tried and quit debt payoff before

- Quick visible progress is important to you

The truth: The best method is the one you'll actually stick to. The difference in total interest paid is usually only a few hundred dollars consistency matters more than perfection.

For more detailed strategies on accelerating your debt payoff, check out our comprehensive guide on 5 proven strategies to pay off debt fast and stick to your budget without stress.

3. Debt Consolidation and Refinancing: Simplify and Save

Consolidating multiple debts into a single loan or refinancing existing loans can simplify payments and potentially lower your interest rate. This is especially useful if you have several high-interest debts.

What is Debt Consolidation?

Debt consolidation combines multiple debts into one new loan or credit line, ideally with a lower interest rate and single monthly payment.

Common consolidation options:

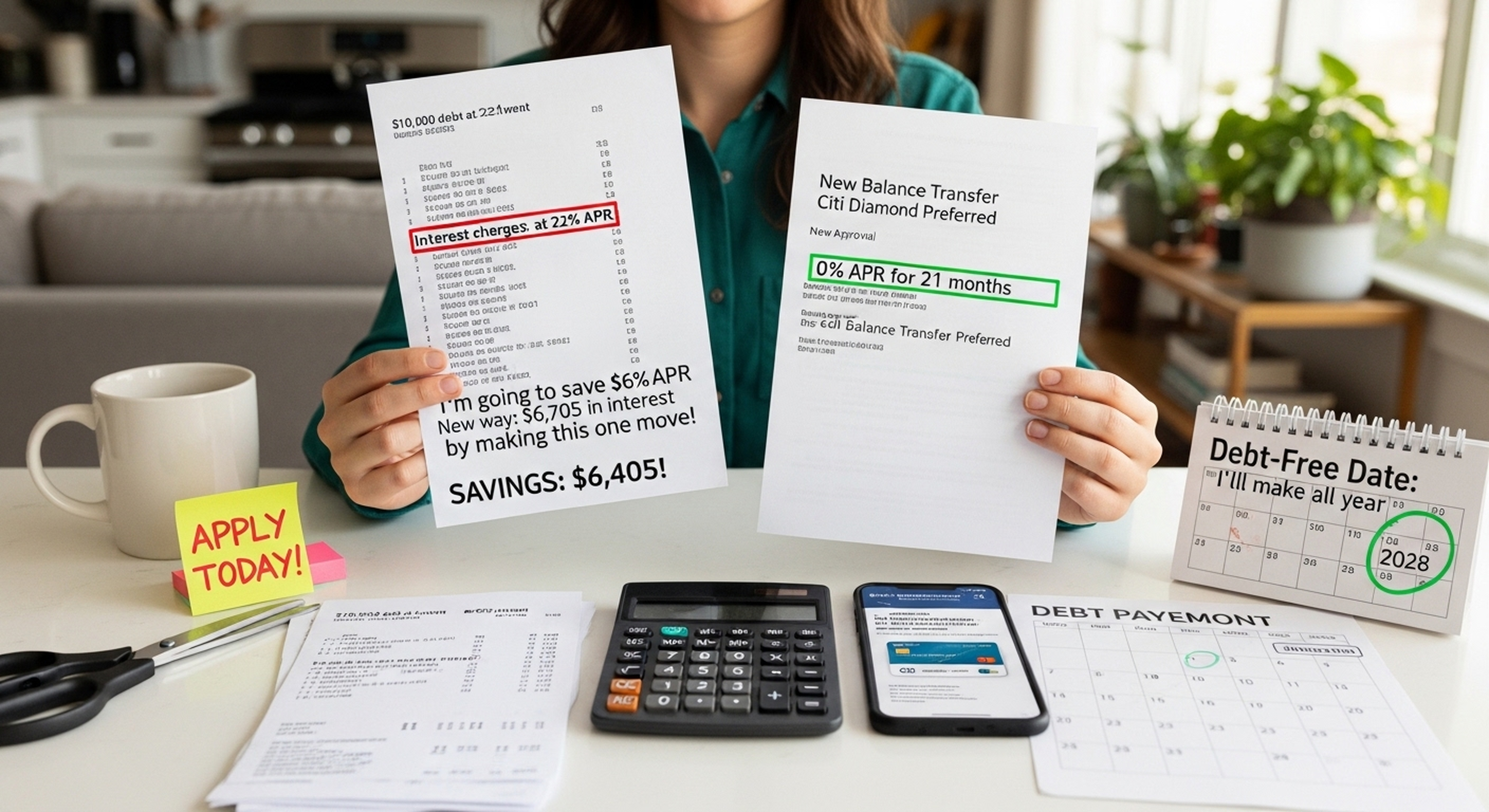

1. Balance Transfer Credit Cards (0% APR Intro)

- How it works: Transfer high-interest balances to a 0% intro APR card (12-21 months)

- Best for: $5,000-15,000 in credit card debt with good credit (680+)

- Typical fee: 3-5% balance transfer fee

- Savings example: $10,000 at 22% APR → 0% for 18 months saves ~$2,000 in interest

- Catch: Must pay off during intro period; rates spike to 20%+ after

2. Personal Consolidation Loans

- How it works: Take out one loan to pay off all credit cards/debts

- Best for: $5,000-50,000 in mixed debt types

- Typical rates: 8-18% APR (based on credit score)

- Savings example: Consolidate three 22% cards into one 12% loan = $1,500+ saved yearly on $15,000

- Pros: Fixed payments, clear payoff date, lower rates

- Cons: Need decent credit; origination fees

3. Home Equity Loans/Lines of Credit (HELOC)

- How it works: Borrow against home equity to pay off debt

- Best for: Homeowners with equity and $20,000+ high-interest debt

- Typical rates: 6-10% APR

- Critical warning: Your home becomes collateral default risk is serious

- Only use if: You're disciplined and won't accumulate new debt

4. Debt Management Plans (through credit counseling)

- How it works: Nonprofit agency negotiates lower rates/payments

- Best for: Those struggling with payments; need professional help

- Typical savings: Interest rates reduced to 8-12%

- Trade-off: Must close credit cards; appears on credit report

When Consolidation Makes Sense

✅ Good reasons to consolidate:

- You'll save significant interest (at least 5% rate reduction)

- Monthly payment becomes more manageable

- You have discipline to not accumulate new debt

- You're committed to the payoff plan

❌ Bad reasons to consolidate:

- To free up credit cards for more spending

- Only for lower monthly payment (extending timeline costs more overall)

- Without addressing root spending problems

- Using home equity without serious consideration

The consolidation trap: Many people consolidate debt, then run up new balances on the freed credit cards. You end up with the new consolidation loan PLUS all the old debt again doubling your problem. Only consolidate if you're committed to not creating new debt.

4. Boost Income to Accelerate Payoff

Sometimes cutting expenses isn't enough. Increasing income even temporarily can dramatically accelerate debt elimination.

Quick income boosts for debt payoff:

- Overtime at current job: $200-500/month extra

- Side hustles: Delivery, rideshare, freelancing = $300-800/month

- Sell unused items: One-time $500-2,000 boost

- Temporary second job: $1,000-2,000/month

Even an extra $400 monthly applied to debt can shorten your payoff timeline by months or years and save thousands in interest.

Need ideas for generating extra cash fast? Our guide on 10 realistic ways to save $1,000 in 30 days includes income-generating strategies you can implement immediately.

5. Seek Professional Help When Needed

If debt feels overwhelming, consider working with a reputable credit counseling agency. These organizations can negotiate with creditors, set up manageable repayment plans, and provide valuable financial guidance.

When to seek professional help:

- Debt exceeds 50% of your annual income

- You're struggling to make minimum payments

- Creditors are calling daily

- You're considering bankruptcy

- Multiple debt types overwhelm you

Reputable resources:

- National Foundation for Credit Counseling (NFCC): Nonprofit counselors

- Financial Counseling Association of America (FCAA): Accredited agencies

- Your bank or credit union: Often offer free financial counseling

Red flags to avoid:

- Companies charging large upfront fees

- "Debt settlement" companies promising to eliminate 50%+ of debt

- Anyone guaranteeing specific results

- Pressure to sign up immediately

Additional Strategies for Debt Management Success

Prioritize High-Interest Debts Aggressively

Focus on paying off debts with the highest interest rates first to minimize overall costs. Every dollar paid toward a 24% credit card saves more than a dollar paid toward a 5% student loan.

Interest rate priority tiers:

- Emergency tier (20%+ APR): Credit cards, store cards, payday loans attack immediately

- High priority (12-20% APR): Personal loans, some car loans target next

- Medium priority (6-12% APR): Some student loans, car loans pay extra when able

- Low priority (under 6% APR): Mortgages, federal student loans minimum payments while focusing elsewhere

Make Consistent Payments Above Minimums

Always pay at least the minimum due on all debts to avoid penalties and protect your credit score. But whenever possible, pay more than the minimum even $20-50 extra makes a difference.

Impact of extra payments:

$5,000 credit card at 20% APR:

- Minimum only ($125): 64 months to pay off, $2,900 interest

- Minimum + $50 ($175): 37 months to pay off, $1,500 interest = $1,400 saved

- Minimum + $100 ($225): 28 months to pay off, $1,100 interest = $1,800 saved

Use Budgeting and Tracking Tools

Leverage apps and online tools to track your progress and stay motivated. Visual progress is powerful for maintaining momentum.

Best debt tracking tools:

- Undebt.it: Free debt payoff planner with multiple methods

- Debt Payoff Planner (app): Visual trackers and motivational milestones

- YNAB (You Need A Budget): Comprehensive budgeting with debt focus

- Mint: Free tracking of all accounts and debts

- Spreadsheets: Customizable and free

Avoid Accumulating New Debt

Refrain from taking on new debt while working on your repayment plan. This is the most common reason debt payoff fails you're bailing water while new leaks keep forming.

Strategies to prevent new debt:

- Freeze credit cards: Literally freeze them in a block of ice

- Remove from online shopping sites: Add friction to impulse purchases

- Use debit/cash only: Envelope system or debit-only spending

- Wait 48 hours rule: For any non-essential purchase over $50

- Build small emergency fund: $1,000 prevents new debt for minor emergencies

Negotiate with Creditors Directly

Many people don't realize creditors will often negotiate, especially if you're struggling. A phone call can save hundreds or thousands.

What you can negotiate:

- Interest rate reduction: "I've been a customer for X years, paying on time. Can you lower my rate from 24% to 18%?"

- Payment plans: If you're behind, negotiate a realistic payment schedule

- Settlement (last resort): Pay lump sum for less than owed (damages credit but clears debt)

- Fee waivers: Request removal of late fees or over-limit fees

Success rate: About 50-60% of people who ask get some form of concession. You'll never get it if you don't ask.

Creating Your Personalized Debt Payoff Plan

Step 1: Inventory and Analyze (Week 1)

- List every debt: creditor, balance, interest rate, minimum payment

- Calculate total debt and monthly minimum payments

- Review credit report for accuracy

- Determine debt-to-income ratio

Step 2: Build Foundation (Weeks 2-8)

- Create bare-bones budget

- Save $1,000 emergency fund as fast as possible

- Continue paying minimums on all debts

Step 3: Choose Method and Execute (Months 2+)

- Select Avalanche or Snowball method

- Calculate how much extra you can pay monthly

- Set up automatic payments

- Attack target debt aggressively

Step 4: Accelerate and Optimize (Ongoing)

- Consider consolidation if beneficial

- Add income boosts when possible

- Negotiate rates with creditors

- Celebrate milestones to maintain motivation

For a comprehensive, detailed action plan, check out our guide on how to pay off $10,000 in debt in 12 months—the strategies apply to any debt amount.

Life After Debt: Maintaining Financial Freedom

Becoming debt-free is just the beginning. The habits and discipline you built during debt payoff become the foundation for long-term wealth building.

Your post-debt financial priorities:

- Complete emergency fund: Build to 3-6 months of expenses

- Retirement investing: Redirect debt payments to 401(k), IRA

- Goal saving: House down payment, travel, major purchases

- Wealth building: Invest in index funds, real estate, or business

The money that once went to debt payments can now build your future. That's the power of debt freedom.

Once your debt is under control, learn how to save for your financial goals effectively and start building real wealth.

Special Considerations: Debt and Investing

A common question: Should I invest while paying off debt, or focus 100% on debt?

The answer depends on interest rates:

Debt above 10% APR: Focus on debt elimination first (after $1,000 emergency fund). The guaranteed return of eliminating 20% credit card debt beats any investment.

Debt 6-10% APR: Split approach—contribute enough to get employer 401(k) match (free money), then focus extra on debt.

Debt under 6% APR: Consider investing while making regular debt payments. Diversified stock market historically returns 8-10% long-term.

Important: Never invest in speculative assets like cryptocurrency while carrying high-interest debt. The risk-reward doesn't make sense. If you're curious about crypto, read our guide on understanding cryptocurrency risks and opportunities in 2025but only after your financial foundation is solid.

Your Debt-Free Future Starts Today

Effective debt management is about making informed choices and using proven strategies to reduce your financial stress. By understanding your debts, creating a realistic budget, and leveraging modern tools and resources, you can work toward a brighter, debt-free future.

The path to debt freedom isn't easy, but it's absolutely achievable. Thousands of people eliminate tens of thousands in debt every year using these exact strategies. You can be one of them.

Remember these key principles:

- Bad debt (high-interest) must be eliminated aggressively

- Choose a payoff method (Avalanche or Snowball) and stick to it

- Budget ruthlessly during debt payoff phase

- Consider consolidation if it saves significant interest

- Boost income when possible to accelerate timeline

- Never accumulate new debt while paying off old

- Seek professional help if truly overwhelmed

Your debt didn't accumulate overnight, and it won't disappear overnight. But with consistency, discipline, and the right strategy, you can be debt-free faster than you think.

The best time to start was yesterday. The second-best time is right now.

🎯 Ready to Take Control of Your Debt?

Download our FREE Debt Payoff Action Kit:

Get our complete Debt Elimination Toolkit including:

- ✅ Debt inventory worksheet

- ✅ Avalanche vs. Snowball calculator

- ✅ Monthly debt tracking spreadsheet

- ✅ Budget templates for aggressive payoff

- ✅ Progress visualization charts

Everything you need to start your debt-free journey today completely free.

What's your biggest debt challenge? Share in the comments below let's support each other on the path to financial freedom.