How to Create a Simple Monthly Budget That Works for You

Feeling overwhelmed by bills, debt, and never-ending expenses? You're not alone but there's a solution. Creating a simple monthly budget can transform your financial life in just 5 steps.

Why Budgeting Is Your Key to Financial Freedom

Let's be real: managing money in today's world feels impossible. Costs keep rising, paychecks stay the same, and there's always something tempting you to spend. The result? Financial stress that keeps you up at night.

Here's a sobering fact: 60% of Americans don't have a budget, and 65% can't cover a $1,000 emergency expense. If you're in this situation, you're dealing with more than just numbers you're dealing with anxiety, uncertainty, and feeling out of control.

But here's the good news: budgeting changes everything.

A well-designed budget isn't about restriction or deprivation. It's about freedom. Freedom to spend guilt-free on things you love, freedom from paycheck-to-paycheck stress, and freedom to build the future you want. Whether you're saving for a house, crushing debt, or just want to stop worrying about money budgeting is your roadmap.

Ready to take control? Let's break down the 5 simple steps to create a monthly budget that actually works.

Budgeting in 2026: What's Different and Why It Matters

If you tried budgeting a few years ago and gave up, 2026 is your fresh start. Here's what's changed:

Economic Reality Check (April 2026)

Inflation has stabilized but costs remain high: After the 2021-2023 inflation surge, prices have leveled off at their new higher baseline. Groceries cost 25% more than 2020, rent is up 30-40% in major cities, and car insurance has nearly doubled. Your budget needs to account for this new reality.

Interest rates are finally dropping: The Federal Reserve started cutting rates in late 2024. As of April 2026, the average credit card APR sits at 19.8% (down from 24%+ in 2023). If you're carrying debt, now is the time to refinance or consolidate before rates potentially rise again.

AI-powered budgeting tools have matured: Budget apps in 2026 use machine learning to predict your spending, automatically categorize expenses with 95%+ accuracy, and send proactive alerts before you overspend. The technology has finally caught up to make budgeting nearly effortless.

Side hustle income is now the norm: 45% of Americans now have a side income stream (up from 34% in 2023). Your 2026 budget should be designed to handle irregular income from freelancing, gig work, or online businesses not just a traditional paycheck. Learn more about managing irregular income with our freelancer budgeting guide.

The "loud budgeting" trend is making it easier: Social media has normalized talking about money. Saying "that's not in my budget" is no longer awkward it's trendy. This cultural shift makes sticking to your budget socially acceptable, even cool.

Bottom line: Budgeting in 2026 requires higher dollar amounts, better tools, and flexible systems. But the fundamentals still work. Let's apply them to your reality.

Step 1: Track Every Dollar Coming In and Going Out

You can't manage what you don't measure. Before you can create a budget, you need to know exactly where your money comes from and where it goes.

Calculate Your Total Monthly Income

Start by listing all your income sources:

- Your primary job salary (use net pay, not gross)

- Side hustles or freelance work

- Passive income (rental properties, dividends, interest)

- Child support or alimony

- Government benefits

- Any other money coming in regularly

Important: If your income varies month to month, calculate your average income from the past 3-6 months. Always use the lower end to avoid overestimating it's better to have extra money than to come up short.

Got side hustle income? Check out our guide on how to budget your side hustle profits to avoid the common mistake of treating irregular income like regular paychecks.

Track Every Single Expense

Now comes the eye-opening part: tracking your spending. For at least one full month (ideally three), record every expense. Yes, every single oneeven that $3 coffee.

Fixed expenses (same amount each month):

- Rent or mortgage

- Car payment

- Insurance (health, car, home, life)

- Loan payments

- Phone and internet bills

- Subscriptions (Netflix, Spotify, gym)

Variable expenses (amounts change):

- Groceries

- Gas and transportation

- Utilities (electric, water, gas)

- Dining out and takeout

- Entertainment and hobbies

- Clothing and personal care

- Household items

2026 app recommendations:

- Monarch Money: Best overall in 2026 ($99/year). Replaced Mint after it shut down in January 2024. Connects to all accounts, beautiful interface, joint budgeting features perfect for tracking every transaction automatically.

- YNAB (You Need A Budget): Still the gold standard for serious budgeters ($14.99/month or $109/year). Now includes AI-powered spending predictions and auto-categorization that learns your habits.

- Rocket Money: Best for canceling subscriptions and negotiating bills. Free tier available, premium is $6-12/month. Saved users an average of $720/year in 2025.

- PocketGuard: Best free option with "In My Pocket" feature showing exactly how much you can safely spend after bills and savings.

- Goodbudget: Best digital envelope system. Free for 10 envelopes, Plus version ($8/month) for unlimited.

Note: Mint by Intuit shut down in January 2024. If you were a Mint user, Monarch Money is the closest replacement with similar features and better design. For a complete comparison, see our 2026 budgeting app rankings.

Prefer pen and paper? That works too just be consistent.

The biggest mistake people make? Forgetting about irregular expenses like annual memberships, car registration, or holiday spending. These "hidden" costs can destroy your budget if you don't plan for them.

Step 2: Categorize Your Spending and Find the Fat

Once you've tracked your expenses, organize them into categories. This reveals your spending patterns and shows where you're bleeding money.

Standard Budget Categories

- Housing: Rent/mortgage, property taxes, home maintenance, utilities

- Transportation: Car payment, insurance, gas, maintenance, public transit

- Food: Groceries, dining out, meal delivery, coffee shops

- Insurance: Health, dental, vision, life, disability

- Healthcare: Copays, medications, medical expenses

- Debt Payments: Credit cards, student loans, personal loans

- Personal: Clothing, haircuts, beauty products, personal care

- Entertainment: Streaming services, hobbies, events, travel

- Savings: Emergency fund, retirement, specific goals

- Miscellaneous: Gifts, donations, unexpected expenses

Needs vs. Wants: The Critical Distinction

Now separate your expenses into two buckets:

Needs = Non-negotiable for survival and basic functioning

Wants = Everything else (even if they feel essential)

This is where people get defensive. "But I need my daily Starbucks!" No, you don't. You want it. And that's okay! Budgeting isn't about eliminating wants it's about being honest about them so you can make intentional choices.

Find Your Money Leaks

Look for patterns in your spending:

- Are you spending $200+ monthly on restaurants?

- Do you have 5 streaming subscriptions you barely use?

- Is that daily $5 coffee adding up to $150 a month?

- Are impulse Amazon purchases draining your account?

These aren't judgments they're opportunities. A single $5 daily habit costs $1,825 per year. That's a vacation, an emergency fund, or a major debt payment.

Struggling with little daily splurges? Read our article on how "little treat culture" is costing you $2,000/year.

Step 3: Set Spending Limits Using the 50/30/20 Rule

Now that you know where your money goes, it's time to tell it where to go instead. The simplest framework? The 50/30/20 rule.

How the 50/30/20 Budget Works

50% = Needs

Half your income covers essentials: housing, utilities, groceries, transportation, insurance, and minimum debt payments. If your rent alone exceeds 50%, that's a red flag you might need cheaper housing or higher income.

30% = Wants

This is your fun money: dining out, entertainment, hobbies, shopping, subscriptions, and vacations. This category makes life enjoyable without derailing your finances.

20% = Savings & Debt Payoff

Put 20% toward building an emergency fund (3-6 months of expenses), retirement savings, and paying down debt beyond minimums.

For income-specific breakdowns with exact dollar amounts, check out our complete budget guidelines with income charts showing how the 50/30/20 rule adjusts for $30K, $50K, $75K, and $100K+ earners.

Real-World Example (2026 Costs)

Let's say you earn $4,000 monthly after taxes in April 2026:

- $2,380 (59.5%) = Needs: (Above ideal 50% realistic for 2026!)

- $1,400 rent (or $1,200 mortgage in lower-cost area)

- $180 utilities (up from $150 in 2024 due to higher energy costs)

- $450 groceries (up from $350-400 in 2023)

- $200 car insurance (doubled since 2020)

- $150 gas (varies by region, $3.20/gallon national average)

- $600 (15%) = Wants: Adjusted down due to higher need costs

- $250 dining out

- $200 entertainment/hobbies

- $150 shopping & miscellaneous

- $1,020 (25.5%) = Savings & Debt:

- $400 emergency fund (prioritize this first!)

- $300 retirement (401k or IRA)

- $320 extra debt payments or investment

2026 Reality Check: Notice how needs exceed 50%? This is common now. Solution: increase income (side hustle), reduce housing costs (roommate/move), or temporarily adjust to 60/20/20 until income grows. The math still works you're just being realistic about current prices.

Sample Monthly Budget Breakdown: $4,000 Income (2026)

| Category | Amount | % of Income |

|---|---|---|

| NEEDS (Target: 50%) | ||

| Rent/Mortgage | $1,400 | 35% |

| Utilities | $180 | 4.5% |

| Groceries | $450 | 11.25% |

| Transportation (insurance + gas) | $350 | 8.75% |

| Needs Subtotal | $2,380 | 59.5% |

| WANTS (Target: 30%) | ||

| Dining Out | $250 | 6.25% |

| Entertainment | $200 | 5% |

| Shopping & Misc | $150 | 3.75% |

| Wants Subtotal | $600 | 15% |

| SAVINGS & DEBT (Target: 20%) | ||

| Emergency Fund | $400 | 10% |

| Retirement | $300 | 7.5% |

| Extra Debt Payment | $320 | 8% |

| Savings & Debt Subtotal | $1,020 | 25.5% |

| TOTAL | $4,000 | 100% |

Key Insight: This example shows needs at 59.5% (above the ideal 50%) which reflects realistic 2026 housing and food costs. The wants category is reduced to compensate while maintaining a strong 25.5% savings rate. Adjust these percentages based on your actual expenses and priorities.

Adjust the Percentages for Your Reality

The 50/30/20 rule isn't gospel it's a guideline. If you're drowning in high-interest debt or live in an expensive city, you might need:

- 60/20/20 if housing costs are high (realistic for 2026 in major cities)

- 50/15/35 if you're aggressively paying off debt

- 50/40/10 if you're just starting and need breathing room

The key is progress, not perfection. Even saving 5-10% is better than nothing.

Set Specific, Measurable Goals

Vague goals like "save more money" fail. Instead, set concrete targets:

- Short-term (3-6 months): Save $1,000 emergency fund, pay off $2,000 credit card

- Mid-term (1-3 years): Save $5,000 for a car down payment, pay off student loans

- Long-term (5+ years): Save $20,000 for a house, build $50,000 retirement fund

Break big goals into monthly chunks. Saving $1,000 in 6 months = $167 per month. That's achievable.

Need help building that initial emergency fund? Our emergency fund guide for tight budgets shows how to save $1,000 with just $5-10/week. And if you want a fun, structured approach, try the 52-week savings challenge to save $1,378 painlessly.

For more strategies on crushing your financial goals, check out our guide on 7 proven ways to save for your goals on a U.S. budget.

Step 4: Choose Your Budgeting Method and Tools

The best budget is the one you'll actually stick to. Here are three proven methods pick what fits your personality and lifestyle.

1. Zero-Based Budgeting (Every Dollar Has a Job)

How it works: Assign every dollar of income to a specific categoryexpenses, savings, or debt until your income minus expenses equals zero.

Example: You earn $3,500 monthly:

- $1,800 needs

- $900 wants

- $600 savings

- $200 extra debt payment

- Total: $3,500 (zero left over)

Best for: Detail-oriented people who want maximum control

Tools: YNAB (You Need A Budget), EveryDollar

Want to dive deeper into this method? Read our complete guide: Zero-based budgeting: Every dollar has a job.

2. Envelope System (Cash-Based Control)

How it works: Withdraw cash and divide it into envelopes labeled with categories (groceries, entertainment, gas). When an envelope is empty, you stop spending in that category.

Example: Put $400 cash in your "groceries" envelope. Once it's gone, you cook from your pantry until next month.

Best for: Overspenders who need physical spending limits

Tools: Physical envelopes or digital versions like Goodbudget

Prefer a digital version? Check out Cash Stuffing 2.0: Digital envelope budgeting system.

3. Automated Budgeting Apps (Set It and Track It)

How it works: Connect your bank accounts to an app that automatically categorizes spending and alerts you when you're over budget.

Best apps for 2026:

- Monarch Money: $99/year, user-friendly, great for beginners (best Mint replacement)

- YNAB: $14.99/month, proactive planning with AI features, best for serious budgeters

- PocketGuard: Free tier available, shows how much "spendable" money you have after bills and savings

- Rocket Money: Free with premium $6-12/month, best for finding and canceling subscriptions

- Spreadsheets: Free, customizable (Google Sheets or Excel)

Best for: Tech-savvy people who want convenience

Tools: Monarch Money, YNAB, PocketGuard, or a simple spreadsheet

Pick One and Commit for 30 Days

Don't overthink it. Choose a method, try it for one month, and adjust if needed. The best system is the one you'll actually use consistently.

Step 5: Review, Adjust, and Stay Flexible

Your budget isn't a set-it-and-forget-it document. It's a living plan that needs regular check-ins and adjustments.

Schedule Monthly Budget Reviews

Set aside 30 minutes at the end of each month to review your budget. Ask yourself:

- Did I stay within my spending limits?

- Which categories did I overspend in?

- Did I hit my savings goals?

- What surprised me this month?

- What should I adjust next month?

If you overspent in one category, don't panic. Adjust by reducing spending in another area next month or finding extra income.

Handle Irregular Expenses with Sinking Funds

Annual or semi-annual expenses destroy budgets. The solution? Sinking funds monthly savings for predictable irregular costs.

Examples:

- Car insurance ($600/year) = Save $50/month

- Holiday gifts ($800/year) = Save $67/month

- Car maintenance ($300/year) = Save $25/month

- Vacation ($1,200/year) = Save $100/month

When the bill comes, you've already saved for it no stress, no scrambling.

Adapt to Life Changes

Life happens. Income changes, expenses shift, emergencies pop up. Your budget should flex with your reality.

Got a raise? Allocate at least 50% to savings or debt before increasing lifestyle spending.

Lost income? Cut wants first, negotiate bills, and pause non-essential subscriptions.

Unexpected expense? Use your emergency fund (that's what it's for!) or temporarily reduce discretionary spending.

Budgeting with a partner? Finances can get complicated when you're managing money together. Our guide on budgeting for couples shows how to merge finances without the fights.

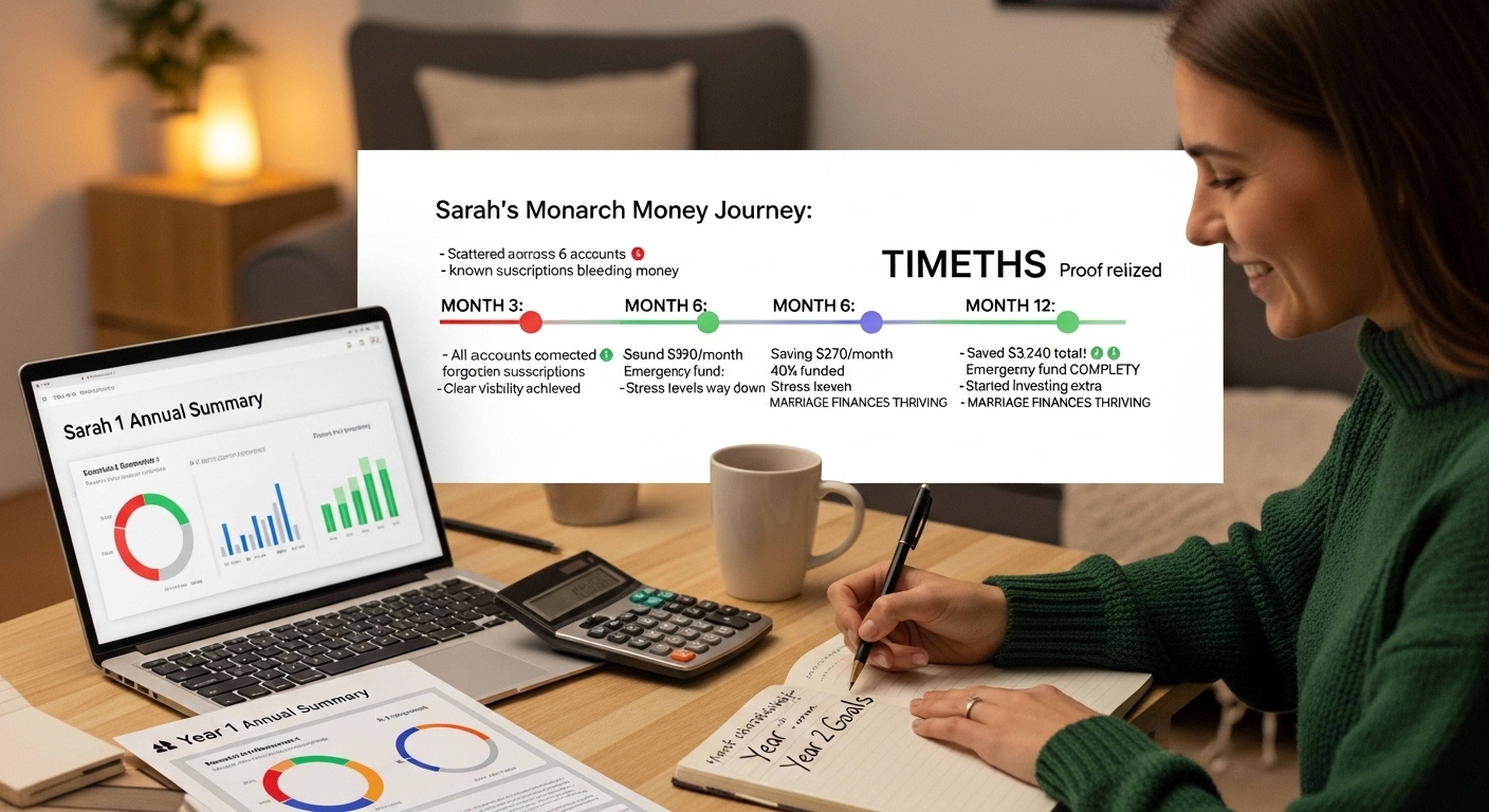

Real-World Success Story

Sarah, a teacher earning $3,500 monthly, noticed she was blowing her clothing budget ($300 vs. $150 budgeted). Instead of giving up, she adjusted: she canceled unused subscriptions ($50 saved), cut dining out ($100 saved), and redirected that $150 to her emergency fund. Within 6 months, she had $1,000 saved her first emergency fund ever.

The lesson? Budgeting isn't about perfection. It's about awareness and adjustment.

7 Bonus Tips to Make Budgeting Easier

1. Automate Everything You Can

Set up automatic transfers to savings on payday. Schedule bill payments to avoid late fees. Automation removes willpower from the equation you save before you can spend.

2. Use the 24-Hour Rule for Impulse Buys

Want to buy something non-essential? Wait 24-48 hours. If you still want it and it fits your budget, buy it guilt-free. Most impulse purchases lose their appeal after a day.

3. Negotiate Your Bills

Call your internet, phone, and insurance providers annually. Say: "I've been a loyal customer for X years. Can you offer me a better rate?" You'll save $20-50 monthly with a 10-minute phone call.

4. Audit Your Subscriptions Quarterly

Review every subscription every 3 months. Cancel what you don't use. Share family plans. Rotate streaming services instead of paying for all of them simultaneously.

5. Use Cash-Back Strategically

Use cash-back credit cards for essentials you'd buy anyway (groceries, gas), then pay off the balance immediately. Never carry a balance interest wipes out rewards.

6. Build in "Fun Money"

Give yourself guilt-free spending money each month. Even $50-100 for whatever you want (no tracking required) prevents budget burnout.

7. Celebrate Your Wins

Hit a savings milestone? Paid off a credit card? Celebrate with a small reward (that fits your budget). Positive reinforcement keeps you motivated.

If you're dealing with debt while trying to budget, read our article on 5 proven strategies to pay off debt fast and stick to your budget. For aggressive debt payoff, check out the debt avalanche method to pay off $15K in 18 months.

Common Budgeting Mistakes to Avoid

1. Being Too Restrictive

If your budget feels like a prison, you'll quit. Build in flexibility and fun money. Sustainable budgets allow enjoyment.

2. Forgetting Irregular Expenses

Annual bills, car maintenance, and holiday spending will destroy your budget if you don't plan for them. Use sinking funds.

3. Not Tracking Spending

You can't improve what you don't measure. Track spending for at least the first 3 months until habits solidify.

4. Giving Up After One Bad Month

You'll overspend sometimes. That's normal. Review what happened, adjust, and keep going. Progress over perfection.

5. Not Planning for Fun

All work and no play makes budgeting unbearable. Always include money for things you enjoy that's what makes life worth living.

Your Budgeting Action Plan: Start Today

You don't need to be perfect. You just need to start. Here's your simple action plan:

Today (30 minutes):

- Calculate your monthly income

- Download a budgeting app or create a spreadsheet

- List all your fixed expenses

This Week:

- Track every expense for 7 days

- Categorize your spending from last month's bank statements

- Identify 2-3 areas where you're overspending

This Month:

- Create your first budget using the 50/30/20 rule

- Set up automatic savings transfers

- Review your budget weekly to stay on track

Next Month:

- Compare your budget to actual spending

- Adjust categories that didn't work

- Celebrate your wins (even small ones!)

Frequently Asked Questions About Monthly Budgeting (2026)

What is the 50/30/20 budget rule?

The 50/30/20 rule divides your after-tax income into three categories: 50% for needs (housing, food, utilities, transportation), 30% for wants (entertainment, dining out, hobbies), and 20% for savings and debt payoff. In 2026, many people adjust to 60/20/20 due to higher housing and food costs caused by inflation. The key is to use it as a guideline and adjust the percentages based on your actual living expenses and financial goals.

What budgeting app is best in 2026?

Monarch Money is the best overall budgeting app in 2026 ($99/year), especially for former Mint users after Mint shut down in January 2024. It offers beautiful design, automatic transaction categorization, and joint budgeting features. YNAB (You Need A Budget) remains the best for serious budgeters ($14.99/month or $109/year) with proactive planning and AI-powered predictions. For a free option, PocketGuard offers the "In My Pocket" feature that shows exactly how much you can safely spend after bills and savings are accounted for.

How much should I budget for groceries in 2026?

For a single person, budget $300-450/month for groceries in 2026. For a couple, expect $550-750/month. For a family of four, plan for $800-1,200/month. These amounts are 20-25% higher than 2020 levels due to inflation. To stay within budget, shop sales and clearance sections, use store brands instead of name brands, meal prep on weekends, make a shopping list and stick to it, and avoid shopping when hungry. Consider using apps like Ibotta or Fetch for cash-back on groceries.

Is budgeting worth it if I'm living paycheck to paycheck?

Yes especially if you're living paycheck to paycheck. Budgeting reveals exactly where every dollar goes, which often uncovers $100-300 in "hidden" spending on subscriptions, dining out, or impulse purchases you didn't realize were adding up. This awareness creates opportunities to redirect money toward building an emergency fund or paying off high-interest debt. Even just tracking your spending for 30 days without making any changes provides eye-opening insights. Budgeting is how you break the paycheck-to-paycheck cycle, not something you do after you've already broken it.

Should I budget before or after taxes?

Always budget using your after-tax income (net pay or take-home pay). The 50/30/20 rule and all budget percentages apply to the money that actually hits your bank account after taxes, health insurance, 401k contributions, and other deductions not your gross salary. Look at your pay stub and find the "net pay" amount that's your budgeting number. If your gross salary is $60,000/year but your net pay is $45,000/year after taxes and deductions, you budget with the $3,750 monthly ($45,000 ÷ 12), not the $5,000 monthly ($60,000 ÷ 12).

How do I budget with irregular income from freelancing or side hustles?

For irregular income, calculate your average monthly income from the past 3-6 months and use the lowest amount as your base budget. Budget your fixed expenses (rent, utilities, insurance) first using that conservative estimate. When you earn above your base amount, allocate the "extra" to savings, irregular expenses (annual bills), and extra debt payments. Consider using a "holding tank" savings account where all income goes first, then pay yourself a consistent "salary" each month. This smooths out the ups and downs of irregular income. For detailed strategies, see our budgeting guide for freelancers.

What if I overspend my budget in one category?

Overspending in a single category doesn't mean your budget has failed. Here's what to do: First, identify why you overspent (unexpected expense, unrealistic budget, or impulse spending). Second, adjust either by cutting spending in another flexible category that same month to compensate, or by adjusting next month's budget if the original amount was too low. Third, use it as a learning opportunity don't beat yourself up. Budgets are meant to be adjusted as you learn your actual spending patterns. The goal is progress over time, not perfection every single month.

Take Control of Your Financial Future Today

Creating a simple monthly budget isn't complicated but it is life-changing. It's the difference between feeling anxious about money and feeling confident. Between hoping you can pay bills and knowing you can. Between living paycheck to paycheck and building real wealth.

You don't need to be a math genius or financial expert. You just need to know where your money goes and make intentional decisions about where you want it to go instead.

The best time to start budgeting was a year ago. The second-best time is right now.

Ready to take action? Download our free 5-Step Budget Planner Spreadsheet a customizable tool that makes budgeting simple and stress-free. No complicated formulas, no confusing categories. Just a straightforward template to help you start managing your money today.

Your financial future starts with one decision: to take control. Make that decision today, and watch your confidence, savings, and peace of mind grow month after month.

What's your biggest budgeting challenge? Drop a comment below and let's solve it together.